Shared Ownership made simple

Shared Ownership is a unique way to buy a home that combines buying and renting. It’s designed to help people who can’t afford a full property purchase. Here we deal with some of the most common issues surrounding Shared Ownership:

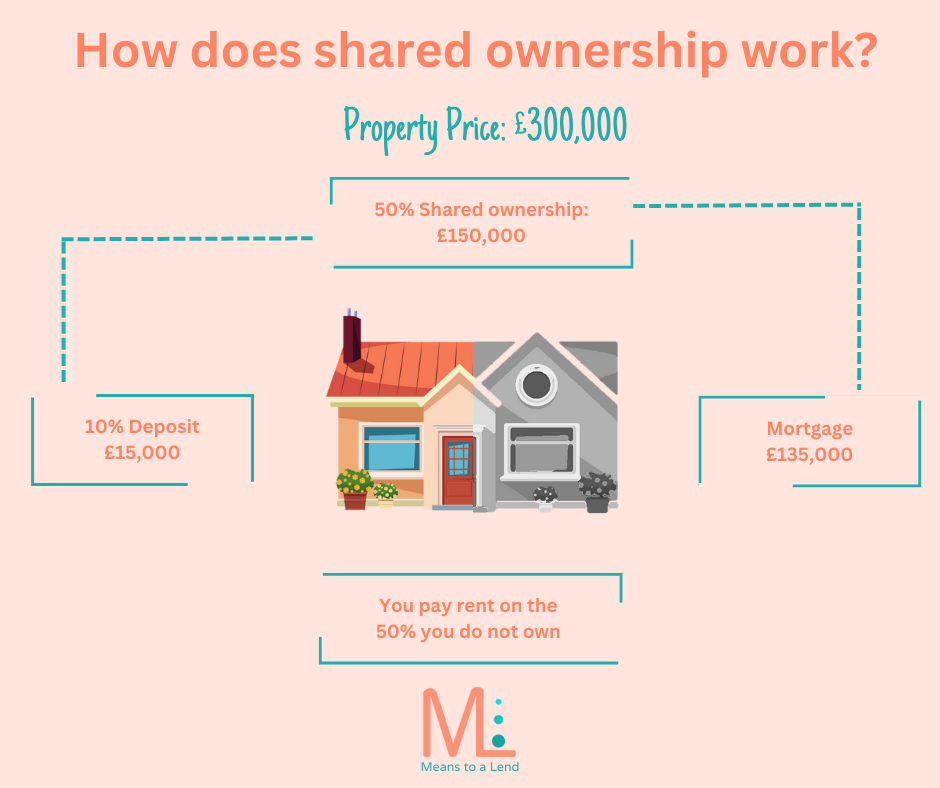

- Affordability: If you think your income isn’t enough to buy a house, Shared Ownership can be a game-changer. You only buy a portion of the property, which means a smaller mortgage and a smaller deposit than with a traditional purchase.

- Property Value: The property’s value is the same as on the open market. Your share is simply a percentage of that value. For instance, if you buy 50% of a £250,000 flat, your deposit and mortgage total £125,000. The housing association owns the rest and charges rent on it.

- Equity Growth: If the property’s value goes up, your equity share grows accordingly. So, if your 50% share increases from £250,000 to £270,000, you gain £10,000.

- Eligibility: To qualify, your combined household income should generally be under £80,000 (or £90,000 in London). You must be a first-time buyer, someone who previously owned a home but can’t afford one now, or a council or housing association tenant.

- Property Share: Shared Ownership offers properties from 25% to 75% ownership. You can gradually buy more until you own the whole property, but the price of the extra share depends on the current value.

- Property Selection: Shared Ownership mostly includes new homes, often part of larger developments. Sometimes, existing Shared Ownership homes become available for resale.

- Extra Rooms: You can buy a property with more bedrooms than you need. However, sub-letting spare rooms is usually not allowed, and rules vary by housing association.

- Leasehold: Shared Ownership properties are leasehold. If you reach 100% ownership, your lease remains but no more rent is payable.

- Previous Ownership: If you owned a home before but now can’t afford one, you can still apply for Shared Ownership.

- Key Worker: Being a key worker isn’t a requirement, but it might be a plus. Some housing associations prioritise key workers, but private sector occupations are eligible too.

- Location: You can apply for properties in areas where you don’t currently live, but preference may be given to those with ties to the area.

- Selling: When you want to sell your Shared Ownership property, the housing association usually has a period to find a buyer. If they can’t, you may decide to find your own estate agent but will need to cover the fees.

- End of Mortgage Deal: When your Shared Ownership mortgage deal ends, you can stay with your current provider or switch to a new one. Switching might get you a better deal or allow you to buy more shares.

- What type of Mortgage can I have? As well as standard residential mortgages, some lenders have products designed specifically for Shared Ownership. If you are over age 55 you can in some cases use a Lifetime Mortgage to purchase the remaining part of the property that you rent.

Shared Ownership makes home ownership achievable for many, offering an alternative path to owning your own place.